|

|

||||

|

|||||

|

|

HOW EMPLOYERS CAN HELP

By Jean Moyer, Corbel

The good news: Retirement savings are up (the 1995 annual average was $2,160 per employee).

The bad news: 40% of the workforce has no pension savings.

The good news: More than three quarters of all eligible employees participate in a 401(k) plan.

The bad news: Increasing numbers of Americans will be unable to maintain their current standard of living in retirement.

Most working Americans know that they'll probably live a third of their life (30 years) in retirement. What they haven't faced up to is how much money they'll need to maintain their current standard of living so as not to be a burden on their children and how to save that much money. Inflation alone could erode half their savings.

Painting a total financial picture as it pertains to an employer's 401(k) plan enables employees to see retirement planning in a much clearer perspective. Corbel developed 401(k) Per$onal, a personalized retirement savings guide that uses employees' current financial data and some generally accepted financial assumptions to create a personalized guide for each employee. The individualized report projects how much income will be needed at retirement, takes into account the progress that has been made so far, and shows how today's investment decisions can affect retirement income. The result is an individualized summary of what options the employee needs to consider to reach his or her goal, and how to use the 401(k) plan to do so.

Here's how it works. The CPA or plan administrator fills out a checklist forecasting financial assumptions (inflation rate, etc.) with the employer. The administrator then pulls employee-specific data from the pension system into an ASCII file and sends the disk and the completed checklist to Corbel. Corbel reviews the data for consistency and validity, inputs the data, and then generates and returns the personalized individual reports to the administrator. The administrator meets with the employer to determine how the reports will be distributed to the plan

The report begins by outlining the employee's personal information such as salary, contribution rate, current savings rate, projected retirement age, etc. Then, as shown in Exhibit 1, it reflects the assumptions made by the plan sponsor and administrator on behalf of the employee base covered by the checklist.

Using these financial forecasts (assumptions) in Exhibit 1 and the employee's personal financial data, the reports are created that show each plan participant how much money he or she will need in retirement. It considers inflation, as well as average investment percentage rates, Social Security, etc. It also shows how much progress the individual has made with 401(k) savings and how much more he or she will need to save by retirement age.

The predicted amount of required savings considers how much the individual will need to maintain his or her current lifestyle over the established retirement period. This is always a jolt to plan participants as the total savings goal seems higher than expected. They are reminded that the goal compensates for inflation and the fact that Social Security and pension funds usually increase at rates less than inflation and are fixed at retirement. Exhibit 2 is a sample from the report showing how the savings goal is attained, the progress made so far, and the savings gap that occurs from the difference.

You'll notice, the employee's current savings rate is projected to retirement age, and the retirement savings gap is computed. This is how much money the employee will need to save to live comfortably in retirement. At this point, the employee can factor in his or her total savings from other sources.

Once the savings gap has been established, the report concentrates on helping the participant make important investment decisions to diminish this gap. Exhibit 3 reveals how different percentages of investment returns and different contribution rates affect the value of savings at retirement. If the contribution rate needed to close the savings gap is more than the employee is capable of adapting, the employee might need to increase his or her investment rate--assume more risk.

The report goes on to discuss inflation (Exhibit 4), how an employee views risk, time horizon (working years left to retirement) vs. risk, and the important role these factors play in an investment

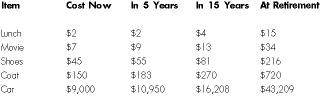

This leads to the topic of diversification to improve overall investment performance. The mix of saving options an employee chooses usually depends on how long he or she will have to invest. Generally, the more time employees have until retirement age, the more aggressive their portfolios can be. Sample investment options illustrating conservative, moderate, and aggressive mixes are included in the report, as well as figures illustrating how a small contribution ($3 a week) can have a big payoff over time (invested at 8%, almost $20,000 in 30 years).

The report concludes by restating the savings goal, calculating the savings gap, and illustrating several variations on how the employee can change his or her savings rate and/or investment strategy to reach the established goal. The report makes it quite clear that all decisions are up to the employee, and that there are no guarantees in any of the suggested strategies. Therefore, 401(k) Per$onal is clearly an educational tool and does not give any specific financial advice.

ERISA Section 404(c) regulations require that plan participants receive extensive information about plan options including plan information, general financial and investment information and asset allocation models which can, but need not be, identified with specific investment options available under the plan. Section 404(c) specifically allows the use of interactive investment materials such as 401(k) Per$onal to stimulate employee savings for retirement.

It's to the plan sponsor's advantage to help individuals to save and invest for retirement, and to make available a comprehensive investment education program. 401(k) Per$onal is a great way to do that and to increase 401(k) plan participation. A recent Merrill Lynch survey reveals that workers whose employers provide retirement planning education have an average annual increase of almost $3,000 in their 401(k) account balances over those whose employers do not provide retirement planning education. They also have a 2.2% higher rate of savings as a percentage of annual income.

If you would like a free sample of a 401(k) Per$onal report, an input checklist, and details of cost, please call Corbel at (800) 326-7235, X1302. *

POWERS OF WITHDRAWAL UPDATE

The power of withdrawal (also known as a Crummey power) is frequently utilized in trust instruments to eliminate or reduce the gift tax on contributions to the trust. A contribution to a trust generally constitutes a gift of a future interest not eligible for the $10,000 annual per donee exclusion ($20,000 where husband and wife elect to split their gifts). However, where a beneficiary has the power to withdraw part or all of the contribution and receives sufficient notice of his or her ability to exercise this withdrawal right, the part of the contribution subject to withdrawal is deemed a gift of a present interest eligible for the annual per donee exclusion. This qualification exists even though it is intended that the beneficiary will not exercise the right of withdrawal and even where the power holder is a minor.

However, the beneficiary must receive actual notice of the right of withdrawal. The best kind of notice, of course, is one that is in writing, since it is evidence that the beneficiary was aware of her or his withdrawal power. Although this is a rather simple precaution to follow, many taxpayers continue to fail to give written notices to beneficiaries or keep copies of such notices in their files. Now there is an IRS private letter ruling that illustrates the costly consequences of insufficient Crummey notices.

In PLR 9532001, the trust document granted the beneficiaries a right of withdrawal over the original transfer to the trust. The trust instrument also provided that the beneficiaries should "be kept reasonably informed" by the trustee of all future gifts to the trust and that they would have withdrawal powers over such gifts as specified in a written notice from the donor to the trustee. However, the beneficiaries had signed a statement on the date of the trust's creation acknowledging receipt of the notice of withdrawal powers and waiving their rights not only to withdraw the initial gift but also to receive any further notices regarding their right of withdrawal as to future gifts.

Not surprisingly, the IRS ruled that all transfers to the trust subsequent to the initial contribution were not eligible for the annual per donee exclusions. A beneficiary must have actual notice of a gift as well as notice of the right to withdraw such gift. Otherwise there is no real and immediate benefit from the transfer that is necessary for it to be a gift of a present interest. Since the trustee did not receive any written notices that the beneficiaries had rights of withdrawal and the beneficiaries had waived their right

All trustees of trusts with withdrawal powers should maintain complete files containing copies of the required notices of withdrawal powers. These notices are routinely requested by estate and gift tax auditors. *

Assumption Retirement Year Value

* You will retire at age 65 In the year 2035.

* Your future pay will increase

4% each year $120,026.

* Your retirement income needs

will be 80% of your final year's pay $96,020.

* Your pension benefit is estimated to be

* Your current plan balance will earn an average of eight percent between now and retirement.

* Social Security benefits will increase an average of three percent each year.

* Inflation (cost of living increases) will average four percent each year.

* After taxes, your investments will earn six percent during retirement.

* Your company matches 50% of the first 3% percent of salary you contribute.

* Your plan limits your contribution rate to a maximum 12% of your salary.

* Your retirement will last 20 years.

Retirement Savings Worksheet

Your current yearly pay projected to age 65 $120,026

Factor for decreased living expenses during retirement x 80%

The estimated income you will need each year for the

20 years of your retirement $96,020

Yearly, Social Security is estimated to contribute $30,137

Yearly, your benefit from pension plans is estimated to be $48,010

The additional yearly income you will have to produce

from your plan investments $17,873

To produce level retirement spending power, you will

need to start your retirement with a total savings of $563,316

$563,316 is your total savings goal.

Your Progress So Far

Total estimated savings you will need at age 65 $563,316

Your current plan balance grown at 8% $65,174

The additional amount you will save by continuing to contribute

1% of pay until retirement. (This assumes average future

investment earnings of 8% and includes company matching

contributions.) $171,350

Your retirement gap (The additional amount your future

investment method will have to produce) $326,793

Your savings gap is $326,793.

Editor:

Contributing Editors:

David Kahn, CPA/PFS

The

CPA Journal is broadly recognized as an outstanding, technical-refereed

publication aimed at public practitioners, management, educators, and

other accounting professionals. It is edited by CPAs for CPAs. Our goal

is to provide CPAs and other accounting professionals with the information

and news to enable them to be successful accountants, managers, and

executives in today's practice environments.

©2009 The New York State Society of CPAs. Legal Notices |

||||

Visit the new cpajournal.com.