|

|

||||

|

|||||

|

|

By Delton L. Chesser and Carlos W. Moore

The demand for traditional services is declining. A multitude of factors are at work that may serve to accelerate the fall-off--technology, competition from non-CPA firms, tax reform. Many CPAs have found success by expanding the financial planning services they offer. The authors report on a survey conducted by them to establish why clients seek the financial planning services of CPAs vs. the competition. They also surveyed the various pricing and compensation arrangements used by those providing financial planning services. The conclusion is that CPAs are a respected provider of financial planning services. The door is open to those seeking to broaden the range of services they

Hawaii was the site of a recent financial planning seminar costing each participant $5,000. Most of the participants earned six-figure incomes. Yet only seven percent had adequate savings to meet their retirement needs. Unfortunately, this group represents how many Americans prepare for retirement--inadequately. More than 62% retiring at age 65 have less than $10,000 a year in retirement income. Forty percent of these people have under $5,000 a year. Few Americans have enough money to comfortably survive many years after retirement because most neither plan in advance nor exercise financial discipline.

People have begun looking to their CPAs for help in solving their financial problems. As a CPA who either offers or is thinking about offering personal financial planning (PFP) services to clients, do you know--

* the reasons why, and their relative importance, clients seek the financial planning services of a CPA?

* CPAs' opinions about pricing PFP services and disclosing certain compensation arrangements?

* about the competition providing PFP services?

In cooperation with the AICPA Planning and Research Department, we collected information for the first two questions by surveying members of the AICPA PFP Division. Questionnaires were mailed to 1,000 randomly selected PFP members. We received 281 responses for a response rate of 28%. For the third question, we conducted a separate survey of 10,000 randomly selected policyholders of a large insurance company. Usable responses totaled 1,734, a 17.3% response rate. The following paragraphs address responses to the two surveys and suggest some benefits to CPAs offering PFP services.

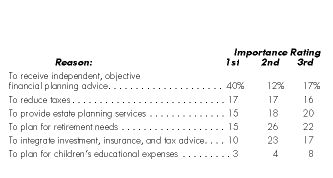

Why Clients Seek PFP Services from CPAs. Previous studies identified reasons why clients typically seek CPAs' financial planning help, but none reported the relative importance of the reasons. We assessed importance by asking CPAs to rank the three most important reasons clients seek these services. The results are presented in Exhibit 1.

Respondents strongly believe independent, objective, advice is the single most important reason for obtaining the PFP services of CPAs. Forty percent ranked this as the most important reason, nearly 21/2 times more frequently than any other reasons. Objectivity and independence are complementary traits that form the basis for the general contract between CPAs and their clients. Objectivity imposes the obligation on all CPAs to be fair and intellectually honest. As a corollary, independence requires a CPA to offer advice free of any conflicts of interest which would bias a recommendation. Both technical competence and moral behavior are necessary for CPAs to fulfill their role as financial advisors. Clearly, a CPA's reputation is his or her most valuable asset because clients demand reliable service.

The second and third most important reasons clients seek PFP services from CPAs are not immediately obvious. Exhibit 1 shows that at least 33% of the respondents ranked four of the five remaining reasons as either first or second. In essence, clients have multidimensional needs that involve complex and comprehensive analysis.

As expected, a major reason clients engage CPAs is for help in reducing taxes. People want less income taxes and more after-tax income. Taxpayers with higher incomes have reason for concern regarding their tax bite. Statistics for 1992, the latest year available, show that the top 10% of all income earners paid well over half (57.5%) of total income taxes even though they earned only 39.2% of total income. The top 10% included taxpayers whose income exceeded $64,560.

Developing a long-term strategy for minimizing a client's tax liability often leads to the discovery of estate planning needs. Attaining the American dream of enjoying a comfortable retirement, leaving a nest egg for the children, and remembering a favorite charity requires careful planning. Most people, for example, realize that contributions to qualified retirement plans grow tax-free. But few know that these assets can be the most highly taxed assets at death, particularly when their accumulations exceed an actuarially determined amount. The actuarial amount represents a comfortable, but not lavish, postretirement lifestyle based on the taxpayer's life expectancy. Excess accumulations can be subject to three different taxes--estate, excise, and income. Because of their expertise in handling tax matters, CPAs can help preserve clients' estates by reducing the liability for "death taxes."

Estate planning's corollary is retirement planning. Most Americans will work for about 40 years and be retired for 20 to 25 years. One of the most difficult and important lifetime financial decisions of most people is, "How much do I need for retirement?" The answer involves complex relationships, such as, the security of long-term employment; the planned age of retirement; the amount an employer contributes to a qualified retirement plan; the rate of inflation; and the retirement plan's rate of return on assets.

Concern about health insurance and long-term health care compounds the planning decision. The current debate on health care, Social Security, and Medicare has propelled the issue of retirement security to the forefront. Most Americans would like to avoid burdening their families during their later years, but they do not understand how to accomplish this objective. The American Association of Retired Persons (AARP) reported that 79% of its members incorrectly believe that Medicare covers a long-term nursing-home stay. Likewise, most people do not realize that employer-provided health insurance will not cover nursing home care. Additionally, typical health insurance inadequately protects against the risk of such catastrophic illnesses as AIDS, cancer, and organ transplants. It takes expert planning to preserve assets against these financial risks and their residual effects.

Because PFP is comprehensive and complex, no one consultant can meet the multidimensional needs of various clients. Effective planning, therefore, requires that someone coordinate the investment, insurance, and tax advice given. Because of their training and ethics, CPAs are in a commanding position to provide this integrative service.

Pricing PFP Services and Disclosing Compensation Arrangements

Respondents to the AICPA survey were asked to indicate their preferences among three options for pricing PFP services: 1) fee-based, 2) commission-based, and 3) combination fee/commission. Overwhelmingly, the respondents (86.6%) preferred the fee-based arrangement. In contrast, less than one percent (.4%) believe CPAs should offer such services only for a commission. Ten percent indicated approval of a combined fee/commission arrangement. Three percent of the respondents expressed no opinion. These results suggest a close link between CPAs' belief why clients select them as financial planners and how CPAs should price their financial planning services. In essence, the respondents imply that fee-based pricing helps reduce conflicts of interest with the CPA.

Exhibit 2 reports the respondents' perceptions about financial planners. We asked respondents to indicate their level of agreement with three statements related to PFP services. Statements 1 and 2 relate to disclosing certain compensation arrangements. For Statement 1, 92.1% of the CPAs agree that financial planners should be required to disclose how much compensation they will receive if clients buy products CPAs recommend. Practitioners expressed very firm support for this disclosure; 83.8% strongly agreed such arrangements should be disclosed, while only 2.6% strongly disagreed with disclosing the compensation.

Responses to Statement 2 show that CPAs even more strongly agree that fee-only planners who split fees with brokers should disclose this arrangement up-front. More than 97% support this disclosure while only 3% voiced moderate disagreement.

Statement 3 reveals that 94.4% of CPAs think financial planners with insurance and brokerage backgrounds emphasize the sale of investment products. The inference may be that these competitors are less concerned with providing objective advice and service than CPAs are. Hopefully, the respondents think CPAs have fewer conflicts of interest with clients than their competitors.

Competition Providing PFP Services

To assess the overall competition providing PFP services, we asked 10,000 randomly selected policyholders of a large insurance company to identify their current financial planners. The choices included attorney, banker, stockbroker, accountant, life insurance agent, friend/relative, or other. For analytical purposes, attorneys, bankers, and stockbrokers were grouped into one response category. The three most frequently used planners were insurance agents (30%), accountants (22%), and attorneys/bankers/stockbrokers (20%). We found, however, as the respondents' levels of income increased so did their preference for accountants. Accordingly, consumers with the highest level of income ($75,000 or more) expressed a significantly greater preference for accountants than for any other PFP provider. The data also revealed that the use of planners increased as income increased.

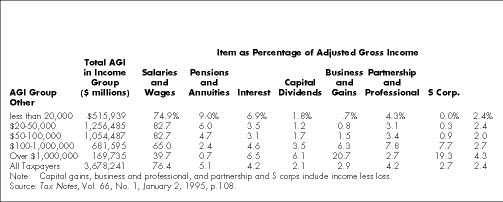

An explanation can be offered as to why higher-income consumers prefer CPAs. Exhibit 3 shows that as income increases, a greater percentage usually comes from sources other than salaries and wages. Proper evaluation of the tax implications of diverse sources requires expertise best provided by CPAs. Thus, a higher level of income creates a greater need for the tax services of CPAs.

Perhaps, the most interesting question addressed is which financial planner will consumers use in the future. When asked whom they would consult for future PFP advice, one third of the respondents indicated accountants were their first choice. Thirty percent selected life insurance agents. Attorneys/bankers/stockbrokers were chosen by 27% of the policyholders. Friends/relatives and others received the remaining 10%. These results place accountants in a very favorable position--the preferred provider of future PFP services.

Consumers' demand for CPAs as financial planners often stems from an existing relationship. For example, while preparing a clients' tax return, the CPA may become aware of the client's need to start saving for retirement. In essence, their practical experience provides ideal on-the-job training for CPAs to become financial planners.

Based on responses from members of the AICPA PFP Division, we compiled a profile of those CPAs who offer PFP services for a fee. The profile reveals that the respondents are experienced practitioners, members of small firms, and primarily male, most have been CPAs for at least 16 years, are between 36 and 55 years old, and belong to firms with five or fewer professionals. Forty-nine percent have earned at least one specialized PFP designation--over one-third have the CFP designation. More than half (54%) have been offering PFP services for at least six years.

Benefits of Offering PFP Services

CPAs can achieve both increased professional fulfillment and economic benefit by helping clients realize a more secure financial future. Knowledge about tax matters and expertise in handling financial affairs make CPAs a natural to serve as advisers. For example, what client does not have a basic tax planning or retirement need? These needs provide a built-in source of new clients. Studies have found that the two most important sources of new PFP clients are existing client relationships and recommendations from current clients. These results confirm that clients value two of the profession's hallmarks--expertise and ethical reputation.

Most CPAs recognize that the profession's unfettered growth era is over and they must adapt to a new marketplace. This new environment is causing CPAs to become broad-based consultants, offering nontraditional services. New services are necessary because accounting is a mature industry, characterized by greater competition and lower profits. PFP services provide an opportunity for helping CPAs adjust to new economic challenges.

Do CPAs need a new paradigm shift to better serve present and future clients? Implementation of a new strategy would be based on a well-developed plan. Effective planning will result in deciding the particular services to offer, identifying potential PFP clients, and matching clients' goals with professional interests. Meeting this need in our graying society will bring both personal and financial rewards. *

Delton L. Chesser, PhD, CPA, is a professor of accounting and Carlos W. Moore, PhD, a professor of marketing, both from Baylor University.

EXHIBIT 3ADJUSTED GROSS INCOME BY SOURCE, 1992

The

CPA Journal is broadly recognized as an outstanding, technical-refereed

publication aimed at public practitioners, management, educators, and

other accounting professionals. It is edited by CPAs for CPAs. Our goal

is to provide CPAs and other accounting professionals with the information

and news to enable them to be successful accountants, managers, and

executives in today's practice environments.

©2009 The New York State Society of CPAs. Legal Notices |

||||

Visit the new cpajournal.com.